Key Values

Decision Support

Strategic and tactical decision making is well supported with a coherent framework and powerful simulation capabilities.

State Of The Art

Risk measurement, credit scoring and rating is made with an up-to-date methodology (survival analysis).

Reflective

Risk-based pricing is developed to balance the quality, profitability and growth objectives with regulatory and market structure constraints.

Ready For Real World

Pricing optimization covers marketing aspects. Lending strategy and pricing logic is determined in the context of the customer engagement cycle.

Customer Oriented

Customer experience is enhanced as they receive real-time loan rates and credit rating with the use of the LPA web application.

Dynamic

A wide range of settings and features are available to target real business needs.

Modularized Features

Interest Rate Engine

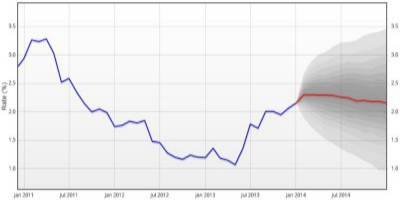

LPA Interest Rate Engine is an advanced econometric model that simulates the yield curve environment of the financial institution. Users are also allowed to incorporate their expert views in the simulation exercise.

Credit Risk Engine

LPA Credit Risk Engine uses an up-to date statistical tool (survival analysis) to model the customer's probability of default on several time horizons from the selected start date. The engine also scores customers and classifies them into risk grades. Credit risk analysis and user-driven model development are compliant with the Basel regulatory standards.

Pricing Engine

LPA Pricing Engine sets the interest rates of loans in a risk-sensitive manner by simultaneously considering the management's risk-return objectives and market share targets and the interest rates offered on similar products by competitors. The software provides a statistically robust framework to discover the true risk-based price of a retail loan.

Competitor Analysis

LPA Competitor Analysis gives real-time and historical insights into the pricing practice of competitors. Heterogeneous, unstructured market data are consolidated on one common platform. The automated information gathering service uses online channels and offers thorough analysis via smart and flexible charting options. The solution enables active market positioning.

Key Portfolio Attributes

LPA Key Portfolio Attributes is a supplementary block that calculates and visualizes the portfolio's nominal cash-flow stream and its various risk metrics such as IFRS 9 compliant expected loss, Basel II and III compliant risk-weighted assets and capital requirement. Key Portfolio Attributes also provides descriptive statistical analysis on the covariates the data set includes.

Data Management

LPA Data Management provides data quality control features in order to facilitate precise financial calculations.